Capitalization Tables for Startup Founders Part 2: Convertible Notes

“Capitalization Tables for Startup Founders” is a three part series that will help new entrepreneurs better understand capitalization tables (“cap tables”). I edited a cap table template from S3 Ventures for this series, which can be downloaded here. Thanks, S3! You can download my specific Excel template (from the video and screenshots below) here — please click the download icon rather than requesting access to the Google Drive file.

Part 1: Pre-Investment | Part 2: Convertible Notes | Part 3: Series A

Prefer video?

Continuing from our pre-investment cap table example, our startup currently has two founders, three employees, an option pool, and no investment. Well, let’s change that last statement.

The date is July 1, 2016, and we successfully received a total investment of $150,000 ($100,000 investment from Angel Investor #1 and $50,000 from Angel #2) in the form of a convertible note.

The most important thing to remember here is that the money received in its current form is a LOAN that will convert into stock at an unspecified future date. Investors will accrue interest and the note will convert into equity at a discounted price (this is the incentive for the angel investors to invest before the Series A investors) at the time of the next round of financing, whenever that may be. For this example, we’ll expect to receive our Series A investment on January 1, 2017.

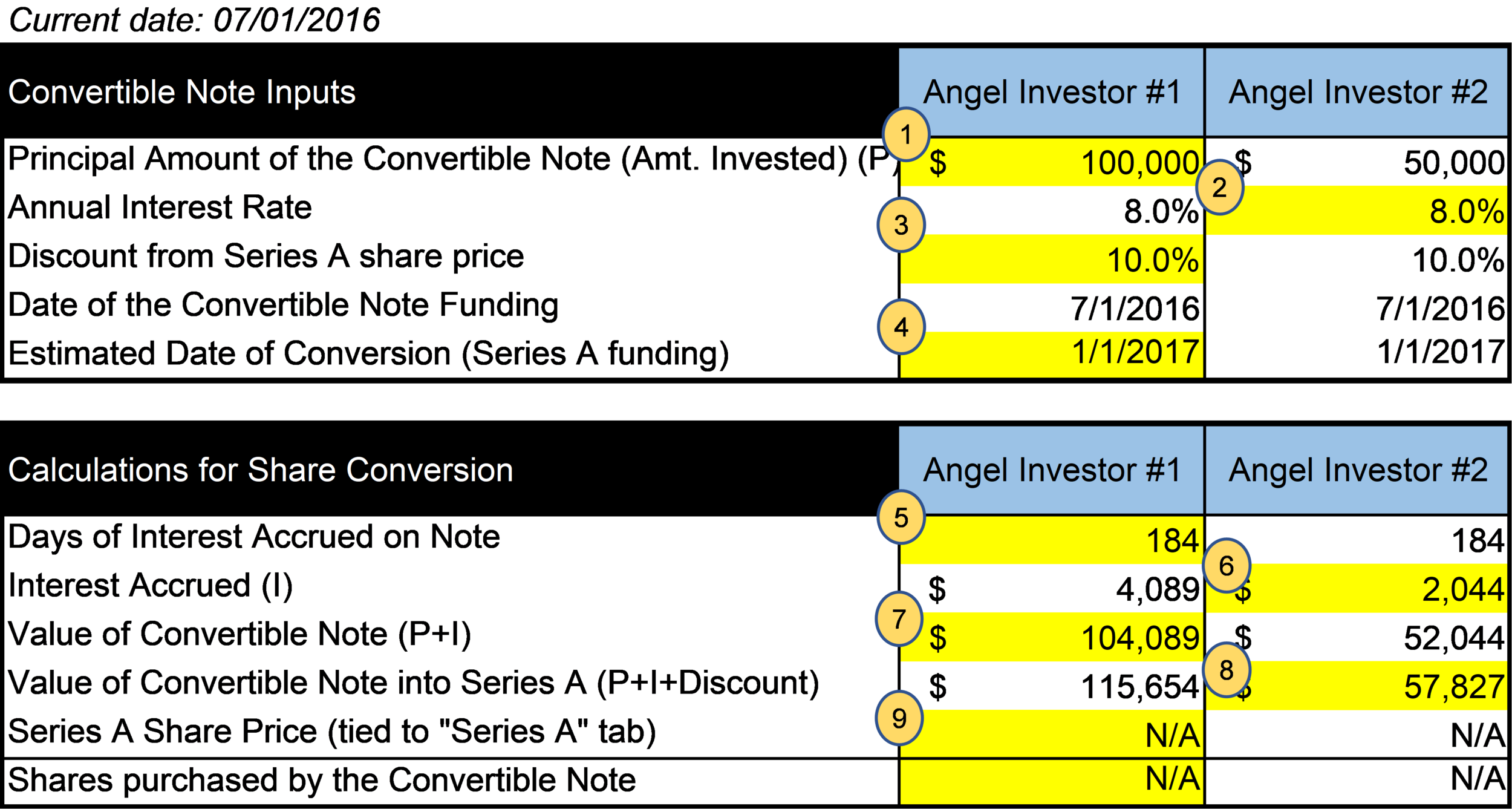

Convertible Note Cap Table

Once again, I’ll walk you through the highlighted cells above:

[1] — Angel Investor #1 gave us an investment of $100,000, as compared to the smaller investment of $50,000 by Angel Investor #2.

[2] — Remember, the convertible note is a loan, and it will accrue interest at an annual rate of 8% until it is converted into equity in the future.

[3] — The incentive for investors who invest in the form of convertible notes is that they are given a discounted per share price, which is derived from the price per share determined in the next round of financing.

To learn more about discount rates and caps of convertible notes, I’ve written about them here.

In our example, the discount is 10%. Notice that we gave both investors the same discount rate. I think it’s a bad idea to give investors differing discount rates without real justification if they provided you capital at the same time.

[4] — As I mentioned earlier, we expect to close our Series A financing on January 1, 2017. Until then, the bottom table will be used as nothing more than a planning tool because we do not yet know our valuation (i.e., price per share) at which our next investment will be completed. Once our Series A round is complete, we’ll revisit this table once again.

I’m including the same table again to minimize your scrolling efforts.

[5] — IF we receive our Series A investment on January 1, 2017, our convertible notes will have accrued interest for 184 days.

[6] — IF the notes accrued interest for 184 days, Angel Investor #2 would have accrued $2,044 of interest [$50,000*((184/360)*8%)].

[7] — 184 days after the initial investment, the total value of Angel Investor #1’s convertible note would be worth $104,089, which is equal to the principal investment of $100,000 plus $4,089 of accrued interest.

[8] — Lastly, prior to the execution of the Series A financing on 1/1/2017, we would determine the total value of each convertible note by including the 10% discount. In this scenario for Angel Investor #2, that value would be $57,827 [$52,044/(100%-10% discount)].

This number is used to calculate how many shares of Series A shares the investor would be issued in the future. For example, if Series A shares are issued at a price of $1 per share, Angel Investor #2 would be given 57,827 shares at the time of conversion.

Note that the longer your convertible notes are outstanding prior to your next round of financing, the more shares these convertible notes will be able to purchase because of additional accrued interest.

[9] — As discussed, these values cannot be determined until the we receive our Series A investment.

Read this over and follow long with your own spreadsheet if it helps. Then, we’ll move on to discussing the Series A investment cap table in my next post.